The Clashing Ideas Over Brazil’s Shrinking Corn Stocks?

Brazil, a global agricultural powerhouse, is facing a perplexing situation: its corn stocks are reportedly shrinking to historic lows, yet conflicting narratives from key agencies are muddying the waters. As of early 2025, Brazil’s own statistics agency, Conab, claims that corn supplies hit their lowest levels in at least 25 years by late February.

Meanwhile, the U.S. Department of Agriculture (USDA) paints a less dire picture, projecting a more gradual decline that won’t reach such extremes until early next year. So, what’s driving these clashing ideas, and what does it mean for Brazil and the global corn market?

The Numbers Tell Different Stories

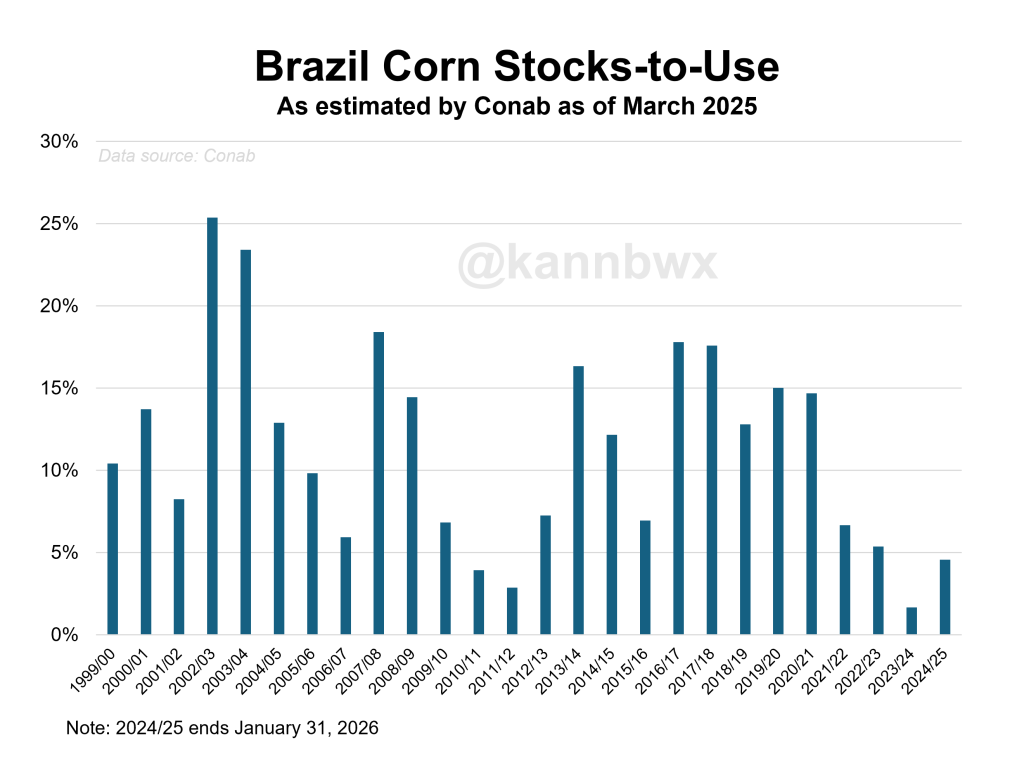

Conab’s data is stark: as of February 2025, Brazil’s corn stocks reportedly dwindled to just 2 million tons, with a stocks-to-use ratio of 1.7%—the lowest since 1999. This suggests a razor-thin buffer against supply shocks, raising alarm bells about potential shortages. Conab anticipates a recovery to 5.5 million tons by January 2026, but that’s still well below the decade-long average of 10.5 million tons.

In contrast, the USDA estimates Brazil’s corn stocks at 7.5 million tons for the same period, down from 10 million tons in 2022-23 but closer to historical norms. The USDA’s stocks-to-use ratio sits at 2.2%, a 42-year low but less catastrophic than Conab’s figures. This discrepancy partly stems from timing: Brazil’s marketing year runs from March to February, while the USDA aggregates data across a broader timeframe, smoothing out short-term dips.

Why the Gap?

Several factors fuel this divide. First, the agencies differ in their export outlooks. Brazil is a corn-exporting giant, often shipping over 40 million tons annually, with the U.S. and China as top buyers. Conab’s leaner stock estimates reflect a more conservative view of export volumes, especially given recent trade turbulence. The USDA, however, remains bullish, expecting Brazil to maintain robust exports despite February typically being a slow month (accounting for just 4% of annual shipments).

Second, domestic consumption plays a role. Brazil’s growing livestock sector and ethanol industry gobble up significant corn volumes—about 70% of its production. Conab may be factoring in higher local demand, while the USDA could be underestimating this pressure. Neither agency has fully clarified these assumptions, leaving room for speculation.

Finally, production forecasts add complexity. Conab recently upped its 2024-25 corn harvest estimate, but trimmed the second crop (safrinha), which dominates exports. Weather challenges, like drought or erratic rains, could further skew outcomes, yet the USDA seems less fazed by these variables so far.

External Pressures: Trade and Policy

Beyond the numbers, external forces are amplifying the debate. U.S. tariffs imposed in early March 2025 on Mexican and Canadian goods—later postponed—sent shockwaves through agricultural markets. Mexico, the top buyer of U.S. corn, might pivot to Brazil, tightening its stocks further. Retaliatory moves, like Canada’s 15% levy on U.S. corn, could also shift trade flows, indirectly pressuring Brazil’s supply.

Domestically, Brazil’s government is responding. Plans to buy 445,000 tons of rice, corn, and beans in 2025 signal a shift toward bolstering food reserves to combat inflation—a departure from past policies. Meanwhile, zeroing import taxes on basic foods aims to ease consumer prices but has sparked criticism from agro-leaders who fear it undercuts local producers without guaranteed relief.

Clashing Ideas, Real Stakes

So, why the clash? It’s a mix of methodological differences, uncertain trade dynamics, and Brazil’s balancing act between feeding its people, fueling its economy, and supplying the world. Conab’s dire view may reflect caution—or a push to justify intervention—while the USDA’s optimism could be a bet on Brazil’s resilience.

The stakes are high. Thin global corn supplies, especially in Brazil, could spike prices, hitting food security in import-dependent nations. For Brazil, depleted stocks risk economic strain if exports falter or domestic needs outstrip supply. Investors, spooked by tariff chaos and recession fears, have already dumped bullish corn bets, signaling unease.

Looking Ahead

As Brazil’s safrinha planting progresses, clarity may emerge. Weather, trade policies, and demand shifts will shape the outcome. For now, the clashing ideas underscore a deeper truth: in a volatile world, even the best data can’t fully predict what’s next for Brazil’s corn. Whether Conab’s alarm or the USDA’s calm prevails, the world is watching—and the margin for error is shrinking fast.

—

The Hotspotorlando News